RSS Feed

RSS Feed by Calculated Risk on 2/11/2013 01:21:00 PM

Monday, February 11, 2013

Fed's Yellen: "A Painfully Slow Recovery for America's Workers"

From Fed Vice Chair Janet Yellen: A Painfully Slow Recovery for America's Workers: Causes, Implications, and the Federal Reserve's Response. Some excerpts on the slow recovery:

In trying to account for why this recovery has been so weak, it is helpful to first consider several important factors that have in the past supported most economic recoveries. By this I don't mean everything that contributes to economic growth, but rather those things that typically play a key role when the U.S. economy is recovering from recession. Think of these as the tailwinds that usually promote a recovery.CR Note: The first missing tailwind is fiscal policy. Even as the Federal government provided some stimulus, state and local governments cut back significant for four consecutive years. And for the last couple of years, we've also seen austerity at the Federal level - and that will probably continue. The good news is the cutbacks at the state and local level are probably mostly over.

The first tailwind I'll mention is fiscal policy. History shows that fiscal policy often helps to support an economic recovery. Some of this fiscal stimulus is automatic, and intended to be. The income loss that individuals and businesses suffer in a recession is partly offset when their tax bills fall as well. Government spending on unemployment benefits and other safety-net programs rises in recessions, helping individuals hurt by the downturn and also supporting consumer spending and the broader economy by replacing lost income. These automatic declines in tax collections and increases in government spending are often supplemented with discretionary fiscal action--tax rate cuts, spending on infrastructure and other goods and services, and extended unemployment benefits. These discretionary fiscal policy actions are typically a plus for growth in the years just after a recession. For example, following the severe 1981-82 recession, discretionary fiscal policy contributed an average of about 1 percentage point per year to real GDP growth over the subsequent three years.

However, discretionary fiscal policy hasn't been much of a tailwind during this recovery. In the year following the end of the recession, discretionary fiscal policy at the federal, state, and local levels boosted growth at roughly the same pace as in past recoveries, as exhibit 3 indicates. But instead of contributing to growth thereafter, discretionary fiscal policy this time has actually acted to restrain the recovery. State and local governments were cutting spending and, in some cases, raising taxes for much of this period to deal with revenue shortfalls. At the federal level, policymakers have reduced purchases of goods and services, allowed stimulus-related spending to decline, and have put in place further policy actions to reduce deficits. ...

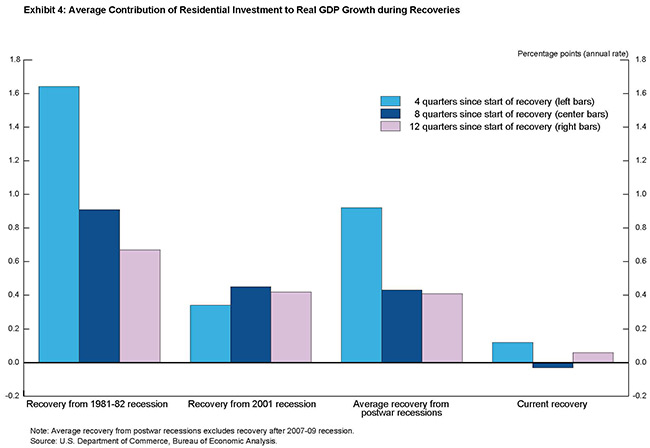

A second tailwind in most recoveries is housing. Residential investment creates jobs in construction and related industries. Before the Great Recession, housing investment added an average of 1/2 percentage point to real GDP growth in the two years after each of the previous four recessions, considerably more than its contribution to growth at other times.

During this recovery, in contrast, residential investment, on net, has contributed very little to growth since the recession ended. The reasons are easy to understand, given the central role that housing played in the Great Recession. Following an extended boom in construction driven in large part by overly loose mortgage lending standards and unrealistic expectations for future home price increases, the housing market collapsed--sales and prices plunged and mortgage credit was sharply curtailed. Tight mortgage credit conditions are continuing to make it difficult for many families to buy homes, despite record-low mortgage interest rates that have helped make housing very affordable. I'm encouraged by recent improvement in the residential sector, but the contribution of housing investment to overall economic activity remains considerably below the average seen in past recoveries, as exhibit 4 shows.

Beyond the direct effects on residential investment, the extraordinary collapse in house prices resulted in a huge loss of household wealth--at last count, net home equity is still down 40 percent, or about $5 trillion, from 2005. ...

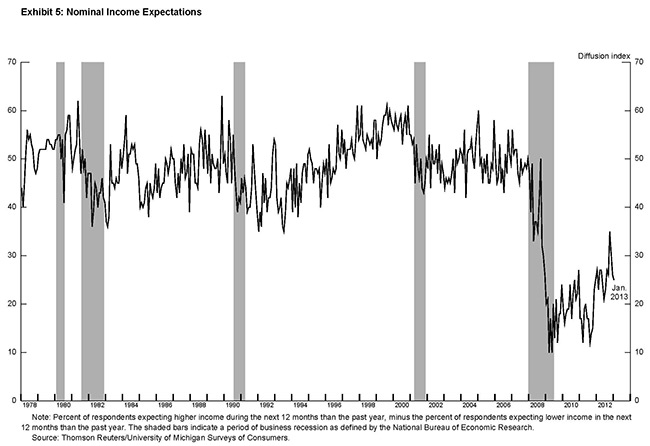

Another important tailwind in most economic recoveries is one that tends to be taken for granted--the faith most of us have, based on history and personal experience, that recessions are temporary and that the economy will soon get back to normal. Even during recessions, households' expectations for income growth tend to be reasonably stable, which provides support for overall spending. In the most recent recession, however, surveys suggest that consumers sharply revised down their prospects for future income growth and have only partially adjusted up their expectations since then (exhibit 5).

The recovery has also encountered some unusual headwinds. The fiscal and financial crisis in Europe has resulted in a euro-area recession and contributed to slower global growth. Europe's difficulties have blunted what had been strong growth in U.S. exports earlier in the recovery by sapping demand worldwide.

The next missing tailwind has been a focus of this blog: Residential investment (RI). RI has finally turned the corner and has started to contribute to the economy. Looking forward, I expect growth to improve over the next few years, although growth will be slowed by the fiscal agreement and other Federal austerity in 2013.

{kind=link}

{kind=link}