RSS Feed

RSS Feed by Calculated Risk on 10/16/2010 07:53:00 PM

Saturday, October 16, 2010

Why did the mortgage servicers use "robo-signers"?

This is a difficult topic to write about because of all the hysteria, emotion and misinformation, but here goes ...

One of the interesting questions with "Foreclosure-Gate" is why several (but not all) mortgage servicers used "robo-signers". This includes GMAC, JPMorganChase, and several other servicers.

First, we have to remember that every foreclosure is a personal tragedy. I support alternatives to foreclosure including modifications, cram-downs, and even short sales. And before another person claims that I support the banks, I fully support fines, sanctions, disbarment, and the investigations by the 50 future governors (the state attorney generals) into "Foreclosure-Gate".

Second, "Foreclosure-Gate" is primarily about "robo-signers". Some people are trying to conflate other sloppy procedures, cost cutting and even MERS (Mortgage Electronic Registration Systems) into "Foreclosure-Gate". This is just confusing readers. All of the servicers who have put foreclosures on hold have done so either because they had "robo-signers" or because they wanted to verify that their processes did not use "robo-signers" (or anything similar). There are valid questions about MERS and other "cost cutting" measures - although most reports I've seen are grossly misinformed - but unfortunately it takes time to get that right (I'll write about that at a later date).

A review: "Robo-signers" are individuals who signed affidavits stating that they had "personal knowledge" of the facts in a foreclosure case, when in fact they did not.

JPM admitted as much this week: "We've identified issues relating to the mortgage foreclosure affidavits and those include signers not having personally reviewed the underlying loan files but instead having relied upon the work of others."

There were also situations of questionable notarization of the affidavits.

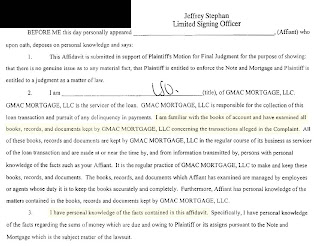

Here is an excerpt that I posted earlier from an affidavit signed by alleged "robo-signer" Jeffrey Stephen of GMAC:

Click on image for larger image in new window.

Click on image for larger image in new window.

I've highlighted a couple of sentences in yellow. Source: Stopa Law Blog

According to the affidavit the affiant claims to have "examined" the details of the transactions in the complaint, and that he has "personal knowledge of the facts contained in the affidavit". In a deposition - according to media reports - the affiant admitted to just signing the documents without verifying the details.

So back to the original question: why did some servicers use "robo-signers"?

I think there are several reasons: the flood of foreclosures, the lack of experienced staff, cost cutting - and also because several of the servicers seemed to use the same service providers to set up their processes (probably the lowest bidder).

Way back in February 2007, Tanta wrote: Mortgage Servicing for UberNerds. Tanta made it clear there are times when servicers are really hurting:

1) When rates are falling and borrowers are refinancing. The servicers get paid a slice of each monthly payment, however their fixed costs are front-loaded. So if people are refinancing too quickly, the servicer doesn't receive enough payments to recoup their fixed costs, and ...

2) When the 90+ day delinquency bucket is increasing rapidly. Although the servicer will eventually recoup the costs for foreclosure, the servicers are usually required to pay property taxes, insurance and all the expenses of foreclosure until the REO is sold.

And right now mortgage rates are falling, and many borrowers are refinancing. And at the same time the 90+ day bucket is at record levels and the servicers are swamped with foreclosure activity. So these are the worst of economic times for servicers.

So, to cut costs and control cash flow, some servicers outsourced foreclosures to the lowest bidders. Here is a possible example from Barry Meir at the NY Times: Foreclosure Mess Draws in the Lawyers Who Handled Them.

And this brings us to another key point that Tanta made in 2007:

[W]hen recovery values in a foreclosure are high (in an RE boom), servicers can noodle along and rack up expenses you didn’t know existed—i.e., shove as much of your “overhead” into FC expenses as you can get away with, since someone else will eventually pay the tab. That’s what we mean when we say that you used to be able to make money off a foreclosure. When the liquidation value starts to approach or drop under the loan amount, on the other hand, investors and insurers start going over those expense reports with a fine-toothed comb, and it can end up in [a] “war”.To no ones surprise, most liquidation values are far below the loan amounts, and investors and insurers are fighting over every servicer expense. This has pushed the servicers to do foreclosures as cheaply as possible (along with the cash flow reasons).

So my guess is a combination of getting swamped with foreclosures, lack of experienced staff, the poor economic environment for servicers, and outsourcing to the lowest bidder, all contributed to the servicers using "robo-signers". This doesn't excuse their behavior - I'm just trying to understand why this happened - and why it happened at more than one servicer.

Of course using the lowest bidders, and ending up with a flawed legal process, is going to lead to even larger battles over expenses between the investors and servicers. So instead of saving money, this is going to be far more expensive for certain servicers.