RSS Feed

RSS Feed by Calculated Risk on 11/01/2008 04:48:00 PM

Saturday, November 01, 2008

The Possible Impact of Contracting Manufacturing in China

From Bloomberg: China Manufacturing Contracts as Crisis Trims Exports

The Purchasing Managers' Index fell to a seasonally adjusted 44.6 last month from 51.2 in September, the China Federation of Logistics and Purchasing said today ... That was the lowest since the gauge was launched in July 2005. A reading below 50 reflects a contraction, above 50 an expansion.As China tries to stimulate their economy, this could have an adverse impact on U.S. interest rates. Let me explain ...

China's cabinet has pledged extra infrastructure spending to stimulate the world's fourth-biggest economy amid the global slowdown. ... ``The government needs effective stimulus measures to spur growth,'' said Wang Qian, a Hong Kong-based economist at JPMorgan Chase & Co. ``The external economic outlook is worsening rapidly.''

Manufacturing contracted in July for the first time since the survey began in 2005. It also shrank in August. The October index was a record low.

First, here is an excerpt from a post I wrote in March 2005:

There is a strong correlation between increases in mortgage debt and increases in the trade deficit. Although the correlation is high, it is very possible that there is no direct linkage, instead the same economic causes that led to higher trade deficits also led to more household borrowing. However, in recent years, with the dramatic increases in mortgage borrowing (far exceeding the increases in GDP) it is reasonable to expect that some of that money is flowing to imports.This led me to correctly predict that as the housing bust picked up steam in the U.S., the trade deficit would peak as a percent of GDP. I also mused about another potential impact of a declining trade deficit - rising intermediate to long term interest rates in the U.S. Here are some diagrams I presented in early 2005:

The implications are important: if the housing market slows down, it will negatively impact both the domestic economy and the economies of our export driven trading partners: China, Japan, S. Korea and others.

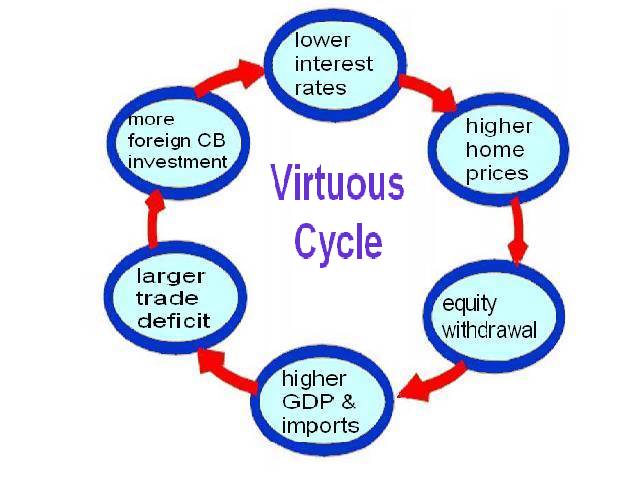

Perhaps we have seen a Virtuous Cycle as depicted in the following diagram:

Click on graph for larger image in new window.

Click on graph for larger image in new window.Starting from the top ... lower interest rates have led to an increase in housing prices. And those higher housing prices have led to an ever increasing equity withdrawal by homeowners. ... it is reasonable to assume that a large percentage of this equity withdrawal has flowed to consumption, increasing both GDP and imports over the last few years. ... it appears mortgage equity withdrawal has been a meaningful contributor to the ever widening trade and current account deficits.

To finance the current account deficit, foreign Central Banks (CBs) have been investing heavily in dollar denominated securities. Some analysts have suggested that these investments have lowered interest rates by between 40 bps and 200 bps (Roubini and Setser: "Will the Bretton Woods 2 Regime Unravel Soon? The Risk of a Hard Landing in 2005-2006")

If these analysts are correct, and foreign CB intervention is lowering treasury yields, then this has also lowered mortgage interest rates ... and the cycle repeats. The result: a Virtuous Cycle with higher housing prices, more consumption and lower interest rates.

As a result of the rapidly increasing housing prices, we are now seeing significant speculation, excessive leverage and poor credit quality of new homebuyers; all the signs of an overheated market. ... What happens if the housing market cools down?

The Vicious Cycle

The following diagram depicts the possible unwinding of the current cycle.

In the possible vicious cycle that I diagrammed, lower home prices would lead to lower equity withdrawal (equity withdrawal has collapsed, see: Q2 2008: Mortgage Equity Withdrawal Plunges to Near Zero) and this would lead to a slow down in GDP growth and lower imports.

In the possible vicious cycle that I diagrammed, lower home prices would lead to lower equity withdrawal (equity withdrawal has collapsed, see: Q2 2008: Mortgage Equity Withdrawal Plunges to Near Zero) and this would lead to a slow down in GDP growth and lower imports.GDP in the U.S. is now contracting, and imports are falling and the trade deficit is shrinking. And as foreign CB invest less in dollar denominated assets (and also try to stimulate their domestic economies) this could lead to higher interest rates for intermediate and long term U.S. assets. As I noted in 2005, the result could be a vicious cycle with higher intermediate and long term rates further depressing the U.S. housing market and consumption.

Although this is very speculative, higher intermediate and long term interest rates in the U.S. for a short period wouldn't be helpful during a recession. This is something to think about as the Chinese economy slows ...