RSS Feed

RSS Feed by Calculated Risk on 5/09/2008 08:00:00 PM

Friday, May 09, 2008

Bank Failure: Some details on ANB Financial

The FDIC closed ANB Financial today with an estimated $214 million hit to the FDIC insurance pool (see previous post). Here are some details from an article earlier this week.

From ArkansasBusiness.com: ANB Past Dues Up 58 Percent (hat tip Steve)

... ANB Financial's loans that are 30 days or more past due were valued at $614.6 million as of March 31, up 58.3 percent from Dec. 31.These small to mid-size institutions mostly missed the residential boom and bust because most residential loans they originated were sold to Wall Street. Instead they focused on construction and development (C&D) and commercial real estate (CRE) loans.

The Bentonville bank's total loan portfolio is about $1.57 billion, so 51 percent of its loans are considered delinquent on one level or another. The majority of those loans - $589.3 million - have been moved all the way into nonaccrual status. A year ago, the bank had $57.9 million in loans that were not accruing interest.

Most of the bank's loans, 77.4 percent, were considered construction and development loans, and 94 percent of the loans are tied to real estate.

C&D loans are especially dangerous. A developer will usually borrow enough to complete the project and make the interest payments, so during development they stay current. However when the developer completes the project - and they can't sell the units - they suddenly stop paying the loan. Notice how the nonaccrual loans increase ten fold over the last year!

Note: for some reason the FDIC hasn't released an "emerging risks" report since late 2006.

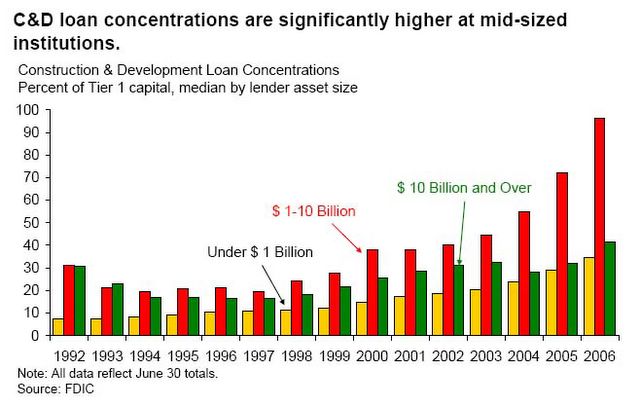

So, from 2006: Look at the concentration of C&D loans in late 2006 (from the FDIC Semiannual Report: Economic Conditions and Emerging Risks in Banking):

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loanAnd that was in late 2006; C&D and CRE lending really went crazy in 2007.

concentrations, especially at institutions with total assets between $1 billion and $10 billion. Four of six Regional Risk Committees expressed some level of concern about CRE lending, in part due to continuing increases in concentrations.

Here come the C&D failures.