RSS Feed

RSS Feed by Calculated Risk on 1/26/2008 06:05:00 PM

Saturday, January 26, 2008

Bank and Thrift Failures

The FDIC announced the first bank failure of 2008 last night. To put that into context, here is a graph of bank and thrift failures since the FDIC was created in 1934.

| Click on graph for larger image. The huge spike in the '80s was due to the S&L crisis. It's interesting to note that even with the failure of almost 3,000 banks and thrifts during the S&L crisis, the overall economy was healthy. |  |

The second graph includes the 1920s and shows that failures during the S&L crisis were far less than during the '20s (before the FDIC was enacted).

The second graph includes the 1920s and shows that failures during the S&L crisis were far less than during the '20s (before the FDIC was enacted).Note how small the S&L crisis appears on this graph!

During the Roaring '20s, 500 bank failures per year was common - even with a booming economy - with depositors typically losing 30% to 40% of their bank deposits in the failed institutions. The number of bank failures soared to 4000 (estimated) in 1933.

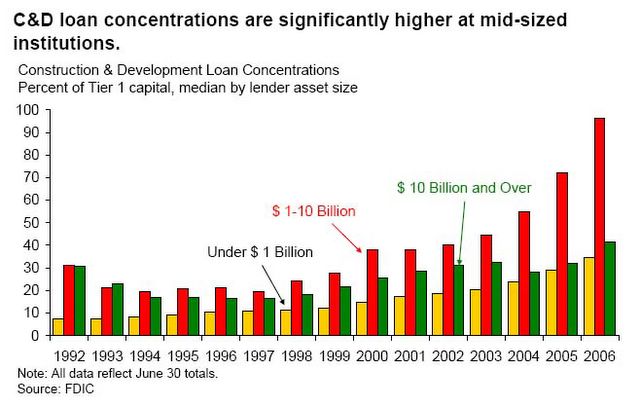

It's important to note that the housing bust hasn't hurt most small banks and institutions, because the banks didn't hold many of the residential mortgages they originated. Instead the small to mid-sized institutions focused on commercial real estate (CRE), construction and development (C&D) and other loans.

From the December 2006 FDIC report: Economic Conditions and Emerging Risks in Banking.

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. ... small and mid-size institutions have been ... assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loan concentrations, especially at institutions with total assets between $1 billion and $10 billion. Four of six Regional Risk Committees expressed some level of concern about CRE lending, in part due to continuing increases in concentrations.Now credit standards are being tightened, and many of these small and mid-sized institutions are seeing rising defaults on their CRE and C&D loans. So 2008 is when we would expect to see more of these small and mid-sized institutions start to fail, but the number of failures will probably be small as compared to the '80s.

Update: Here is an addition from the

Atlanta's residential bust is rapidly becoming a financial disaster on a par with the Savings and Loan Crisis of the 1980s.The article (subscription) reports that at the peak of the S&L crisis, the non-performing loans reached 4.4% for Altanta based banks (compared to 2.2% at the end of Q3 2007). However the article quotes several bankers and industry analysts that believe the percent of non-performing loans increased significantly in Q4, and will rise sharply in 2008.