RSS Feed

RSS Feed by Calculated Risk on 11/30/2022 08:54:00 PM

Wednesday, November 30, 2022

Thursday: Personal Income & Outlays, Unemployment Claims, ISM Mfg, Construction Spending, Vehicle Sales

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 235 thousand initial claims, down from 240 thousand last week.

• Also, at 8:30 AM, Personal Income and Outlays, October 2022. The consensus is for a 0.4% increase in personal income, and for a 0.8% increase in personal spending. And for the Core PCE price index to increase 0.3%. PCE prices are expected to be up 6.2% YoY, and core PCE prices up 5.0% YoY.

• At 10:00 AM, ISM Manufacturing Index for November. The consensus is for 50.0%, down from 50.2%.

• Also, at 10:00 AM, Construction Spending for October. The consensus is for 0.3% decrease in spending.

• All day: Light vehicle sales for November. The consensus is for 14.9 million SAAR in November, unchanged from the BEA estimate of 14.9 million SAAR in October (Seasonally Adjusted Annual Rate).

Fed's Beige Book: "Apartment leasing started to slow"

by Calculated Risk on 11/30/2022 04:41:00 PM

Fed's Beige Book "This report was prepared at the Federal Reserve Bank of Boston based on information collected on or before November 23rd, 2022."

Economic activity was about flat or up slightly since the previous report, down from the modest average pace of growth in the prior Beige Book period. Five Districts reported slight or modest gains in activity, and the rest experienced either no change or slight-to-modest declines. Interest rates and inflation continued to weigh on activity, and many contacts expressed greater uncertainty or increased pessimism concerning the outlook. Nonauto consumer spending was mixed but, on balance, eked out slight gains. Inflation pushed low-to-moderate income consumers to substitute increasingly to lower-priced goods. Travel and tourism contacts, by contrast, reported moderate gains in activity, as restaurants and high-end hospitality venues enjoyed robust demand. Auto sales declined slightly on average, but sales increased significantly in a few Districts in response to higher inventories. Manufacturing activity was mixed across Districts but up slightly on average. Demand for nonfinancial services was flat overall but softened in some Districts. Higher interest rates further dented home sales, which declined at a moderate pace overall but fell steeply in some Districts; apartment leasing started to slow, as well. Residential construction slid further at a modest pace, while nonresidential construction was mixed but down slightly on average. Commercial leasing weakened slightly, and office vacancies edged up. Bank lending saw modest further declines amid increasingly weak demand and tightening credit standards. Agricultural conditions were flat or up a bit, and energy sector activity increased slightly on balance.

Employment grew modestly in most districts, but two Districts reported flat headcounts and labor demand weakened overall. Hiring and retention difficulties eased further, although labor markets were still described as tight. Scattered layoffs were reported in the technology, finance, and real estate sectors.

emphasis added

Fed Chair Powell: "The time for moderating the pace of rate increases may come as soon as the December meeting"

by Calculated Risk on 11/30/2022 01:38:00 PM

From Fed Chair Powell: Inflation and the Labor Market. Excerpts:

Today I will offer a progress report on the Federal Open Market Committee's (FOMC) efforts to restore price stability to the U.S. economy for the benefit of the American people. The report must begin by acknowledging the reality that inflation remains far too high. My colleagues and I are acutely aware that high inflation is imposing significant hardship, straining budgets and shrinking what paychecks will buy. This is especially painful for those least able to meet the higher costs of essentials like food, housing, and transportation. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all.

...

Housing services inflation measures the rise in the price of all rents and the rise in the rental-equivalent cost of owner-occupied housing. Unlike goods inflation, housing services inflation has continued to rise and now stands at 7.1 percent over the past 12 months. Housing inflation tends to lag other prices around inflation turning points, however, because of the slow rate at which the stock of rental leases turns over.2 The market rate on new leases is a timelier indicator of where overall housing inflation will go over the next year or so. Measures of 12-month inflation in new leases rose to nearly 20 percent during the pandemic but have been falling sharply since about midyear (figure 3).

As figure 3 shows, however, overall housing services inflation has continued to rise as existing leases turn over and jump in price to catch up with the higher level of rents for new leases. This is likely to continue well into next year. But as long as new lease inflation keeps falling, we would expect housing services inflation to begin falling sometime next year. Indeed, a decline in this inflation underlies most forecasts of declining inflation.

...

Returning to monetary policy, my FOMC colleagues and I are strongly committed to restoring price stability. After our November meeting, we noted that we anticipated that ongoing rate increases will be appropriate in order to attain a policy stance that is sufficiently restrictive to move inflation down to 2 percent over time.

Monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting. Given our progress in tightening policy, the timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level. It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.

emphasis added

Inflation Adjusted House Prices 3.3% Below Peak

by Calculated Risk on 11/30/2022 10:48:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 3.3% Below Peak

Excerpt:

It has been over 16 years since the bubble peak. In the Case-Shiller release yesterday, the seasonally adjusted National Index (SA), was reported as being 62% above the bubble peak in 2006. However, in real terms, the National index (SA) is about 12% above the bubble peak (and historically there has been an upward slope to real house prices). The composite 20, in real terms, is about 3% above the bubble peak.

Both indexes have declined for four consecutive months in real terms (inflation adjusted).

People usually graph nominal house prices, but it is also important to look at prices in real terms. As an example, if a house price was $200,000 in January 2000, the price would be almost $338,000 today adjusted for inflation (69% increase). That is why the second graph below is important - this shows "real" prices. ...

The second graph shows the same two indexes in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices. In real terms, the National index is 3.3% below the recent peak, and the Composite 20 index is 4.4% below the recent peak in 2022.

In real terms, house prices are still above the bubble peak levels. There is an upward slope to real house prices, and it has been over 16 years since the previous peak, but real prices are historically high.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

NAR: Pending Home Sales Decreased 4.6% in October, Year-over-year Down 37%

by Calculated Risk on 11/30/2022 10:11:00 AM

From the NAR: Pending Home Sales Declined 4.6% in October

Pending home sales slid for the fifth consecutive month in October, according to the National Association of REALTORS®. Three of four U.S. regions recorded month-over-month decreases, and all four regions recorded year-over-year declines in transactions.This was close to the expected decline for this index. Note: Contract signings usually lead sales by about 45 to 60 days, so this would usually be for closed sales in November and December.

The Pending Home Sales Index (PHSI), a forward-looking indicator of home sales based on contract signings, sank 4.6% to 77.1 in October. Year-over-year, pending transactions slipped by 37.0%. An index of 100 is equal to the level of contract activity in 2001.

"October was a difficult month for home buyers as they faced 20-year-high mortgage rates," said NAR Chief Economist Lawrence Yun. "The West region, in particular, suffered from the combination of high interest rates and expensive home prices. Only the Midwest squeaked out a gain."

"The upcoming months should see a return of buyers, as mortgage rates appear to have already peaked and have been coming down since mid-November."

...

The Northeast PHSI sank 4.3% from last month to 68.7, a fall of 29.5% from October 2021. The Midwest index increased 3.3% to 83.5 in October, a decrease of 32.1% from one year ago.

The South PHSI dropped 6.4% to 90.6 in October, falling 38.2% from the prior year. The West index slipped by 11.3% in October to 55.6, sinking 46.2% from October 2021.

emphasis added

BLS: Job Openings Decreased to 10.3 million in October

by Calculated Risk on 11/30/2022 10:06:00 AM

From the BLS: Job Openings and Labor Turnover Summary

The number of job openings edged down to 10.3 million on the last business day of October, the U.S. Bureau of Labor Statistics reported today. Over the month the number of hires and total separations changed little at 6.0 million and 5.7 million, respectively. Within separations, quits (4.0 million) and layoffs and discharges (1.4 million) changed little.The following graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

emphasis added

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for October the employment report this Friday will be for November.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are usually pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

The spike in layoffs and discharges in March 2020 is labeled, but off the chart to better show the usual data.

Jobs openings decreased in October to 10.334 million from 10.687 million in September.

The number of job openings (black) were down 7% year-over-year.

Quits were down 3% year-over-year. These are voluntary separations. (See light blue columns at bottom of graph for trend for "quits").

Q3 GDP Growth Revised Up to 2.9% Annual Rate

by Calculated Risk on 11/30/2022 08:33:00 AM

From the BEA: Gross Domestic Product (Second Estimate) and Corporate Profits (Preliminary), Third Quarter 2022

Real gross domestic product (GDP) increased at an annual rate of 2.9 percent in the third quarter of 2022, according to the "second" estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP decreased 0.6 percent.Here is a Comparison of Second and Advance Estimates. PCE growth was revised up from 1.4% to 1.7%. Residential investment was revised down from -26.4% to -26.8%.

The GDP estimate released today is based on more complete source data than were available for the "advance" estimate issued last month. In the advance estimate, the increase in real GDP was 2.6 percent. The second estimate primarily reflected upward revisions to consumer spending and nonresidential fixed investment that were partly offset by a downward revision to private inventory investment. Imports, which are a subtraction in the calculation of GDP, decreased more than previously estimated

...

Real gross domestic income (GDI) increased 0.3 percent in the third quarter, in contrast to a decrease of 0.8 percent in the second quarter (revised). The average of real GDP and real GDI, a supplemental measure of U.S. economic activity that equally weights GDP and GDI, increased 1.6 percent in the third quarter, in contrast to a decrease of 0.7 percent (revised) in the second quarter.

emphasis added

ADP: Private Employment Increased 127,000 in November

by Calculated Risk on 11/30/2022 08:21:00 AM

Private sector employment increased by 127,000 jobs in November and annual pay was up 7.6 percent year-over-year, according to the November ADP® National Employment ReportTM produced by the ADP Research Institute® in collaboration with the Stanford Digital Economy Lab (“Stanford Lab”)This was below the consensus forecast of 200,000. The BLS report will be released Friday, and the consensus is for 200 thousand non-farm payroll jobs added in November.

The jobs report and pay insights use ADP’s fine-grained anonymized and aggregated payroll data of over 25 million U.S. employees to provide a representative picture of the labor market. The report details the current month’s total private employment change, and weekly job data from the previous month. ADP’s pay measure uniquely captures the earnings of a cohort of almost 10 million employees over a 12-month period.

“Turning points can be hard to capture in the labor market, but our data suggest that Federal Reserve tightening is having an impact on job creation and pay gains,” said Nela Richardson, chief economist, ADP. “In addition, companies are no longer in hyper-replacement mode. Fewer people are quitting and the post-pandemic recovery is stabilizing.”

emphasis added

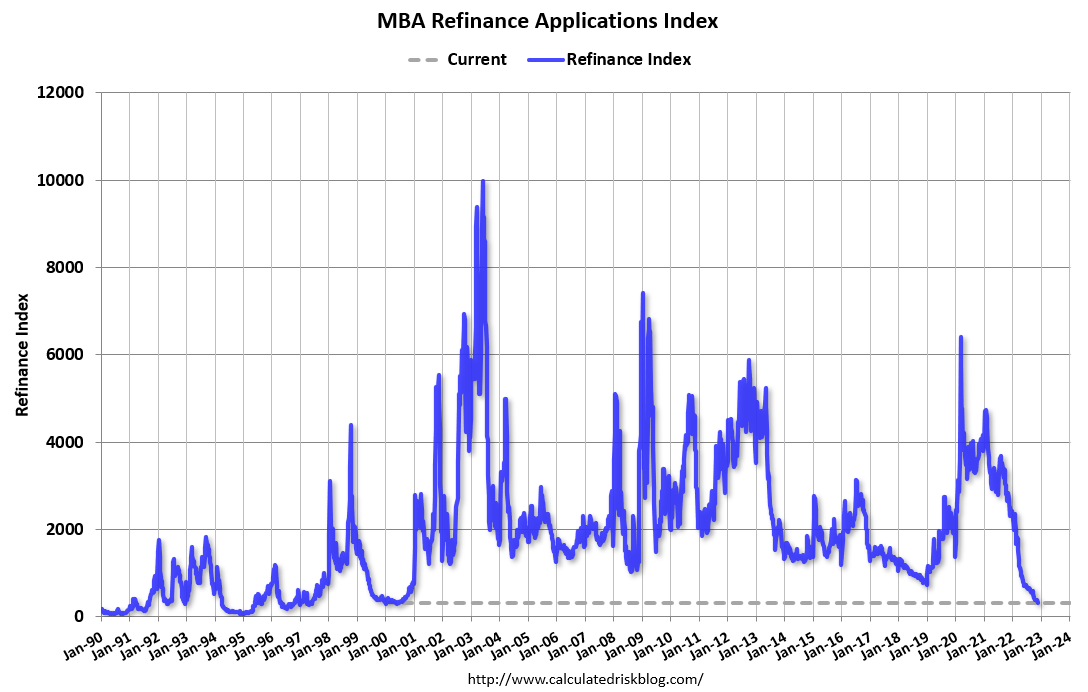

MBA: Mortgage Applications Decrease in Latest Weekly Survey

by Calculated Risk on 11/30/2022 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 25, 2022. This week’s results include an adjustment for the observance of the Thanksgiving holiday.

... The Refinance Index decreased 13 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 4 percent from one week earlier. The unadjusted Purchase Index decreased 31 percent compared with the previous week and was 41 percent lower than the same week one year ago.

“Mortgage rates declined again last week, following bond yields lower. The 30-year fixed mortgage rate decreased to 6.49 percent and has now fallen 57 basis points over the past four weeks. Additionally, mortgage rates for most other loan types declined,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “The economy here and abroad is weakening, which should lead to slower inflation and allow the Fed to slow the pace of rate hikes. Purchase activity increased slightly after adjusting for the Thanksgiving holiday, but the decline in rates was still not enough to bring back refinance activity. Refinance applications fell another 13 percent, and the refinance share of applications was at 26 percent. Both measures were at their lowest levels since 2000.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 6.49 percent from 6.67 percent, with points remaining at 0.68 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply this year.

The refinance index is at the lowest level since the year 2000.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 41% year-over-year unadjusted.

According to the MBA, purchase activity is down 41% year-over-year unadjusted.The purchase index is just below the pandemic low and up slightly from the lowest level since 2015.

Note: Red is a four-week average (blue is weekly).

Note: Red is a four-week average (blue is weekly).

Tuesday, November 29, 2022

Wednesday: GDP, ADP Employment, Job Openings, Pending Home Sales, Fed Chair Powell and More

by Calculated Risk on 11/29/2022 09:23:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:15 AM: The ADP Employment Report for November. This report is for private payrolls only (no government). The consensus is for 200,000 jobs added, down from 239,000 in October.

• At 8:30 AM: Gross Domestic Product (Second Estimate) and Corporate Profits (Preliminary), 3rd Quarter 2022. The consensus is that real GDP increased 2.7% annualized in Q3, up from the advance estimate of 2.6% in Q3.

• At 9:45 AM: Chicago Purchasing Managers Index for November.

• At 10:00 AM ET: Job Openings and Labor Turnover Survey for October from the BLS.

• At 10:00 AM: Pending Home Sales Index for October. The consensus is for a 5.0% decrease in the index.

• At 10:30 AM: (likely) FDIC Quarterly Banking Profile, Third quarter.

• At 1:30 PM: Speech, Fed Chair Jerome Powell, Economic Outlook, Inflation, and the Labor Market, At the Brookings Institution, 1775 Massachusetts Avenue N.W., Washington, D.C.

• At 2:00 PM: the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.