RSS Feed

RSS Feed by Calculated Risk on 10/10/2021 08:11:00 AM

Sunday, October 10, 2021

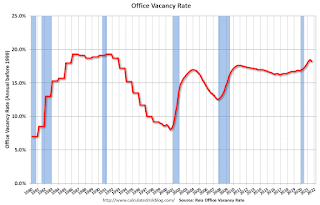

Reis: Office and Mall Vacancy Rates Decreased Slightly in Q3

Reis reported the office vacancy rate was at 18.2% in Q3, down from 18.5% in Q2, and up from 17.4% in Q3 2020.

The previous quarter (back in Q2) saw the highest vacancy rate for offices since the early '90s (following the S&L crisis).

Click on graph for larger image.

Click on graph for larger image.

The first graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual).

Reis also reported that office effective rents increased slightly in Q3; this followed five consecutive quarter with declining rents.

Click on graph for larger image.

Click on graph for larger image.The first graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual).

The office vacancy rate was elevated prior to the pandemic, and moved up during the pandemic.

Reis also reported that office effective rents increased slightly in Q3; this followed five consecutive quarter with declining rents.

The second graph shows the regional and strip mall vacancy rate starting in 1980 (prior to 2000 the data is annual).

For Neighborhood and Community malls (strip malls), the vacancy rate was 10.4% in Q3, down from 10.5% in Q2, and unchanged from 10.4% in Q3 2020.

For Regional malls, the vacancy rate was 11.2% in Q3, down from 11.5% in Q2, and up from 10.1% in Q3 2020.

For Neighborhood and Community malls (strip malls), the vacancy rate was 10.4% in Q3, down from 10.5% in Q2, and unchanged from 10.4% in Q3 2020.

For Regional malls, the vacancy rate was 11.2% in Q3, down from 11.5% in Q2, and up from 10.1% in Q3 2020.

Reis reported that mall effective rents increased slightly in Q3, after stabilizing in Q2. This followed five consecutive quarters will declining rents.

All vacancy data courtesy of Reis

All vacancy data courtesy of Reis

Saturday, October 09, 2021

Newsletter Articles this Week

by Calculated Risk on 10/09/2021 02:11:00 PM

At the Calculated Risk Newsletter this week:

• Measuring Rents How quickly are rents increasing? And how will this impact measures of inflation?

• On Private Lenders Raising the "Conforming Loan Limit" The Official Announcement for 2022 will be in Late November.

• 1st Look at Local Housing Markets in September Denver, Las Vegas and San Diego.

• Homebuilder Comments in September: “Supply chain, supply chain, supply chain." "Monthly price hikes no longer the norm. Some of the hottest markets sounding toppy."

• 2nd Look at Local Housing Markets in September Adding Memphis, Nashville, North Texas (Dallas), Northwest (Seattle), Sacramento and Santa Clara (San Jose).

This will usually be published several times a week, and will provide more in-depth analysis of the housing market.

The blog will continue as always!

You can subscribe at https://calculatedrisk.substack.com/ Currently all content is available for free - and some will always be free - but please subscribe!.

You can subscribe at https://calculatedrisk.substack.com/ Currently all content is available for free - and some will always be free - but please subscribe!.

Schedule for Week of October 10, 2021

by Calculated Risk on 10/09/2021 08:11:00 AM

The key economic reports this week are September CPI and Retail Sales.

For manufacturing, the October New York Fed survey will be released this week.

Columbus Day Holiday: Banks will be closed in observance of Columbus Day. The stock market will be open. No economic releases are scheduled.

6:00 AM: NFIB Small Business Optimism Index for September.

10:00 AM: Job Openings and Labor Turnover Survey for August from the BLS.

10:00 AM: Job Openings and Labor Turnover Survey for August from the BLS. This graph shows job openings (yellow line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in July to 10.934 million from 10.185 million in June. This is a new record high for this series.

The number of job openings (yellow) were up 63% year-over-year. Quits were up 25% year-over-year.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The Consumer Price Index for September from the BLS. The consensus is for a 0.3% increase in CPI, and a 0.3% increase in core CPI.

2:00 PM: FOMC Minutes, Meeting of September 21-22, 2021

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 315 thousand initial claims, down from 326 thousand last week.

8:30 AM: The Producer Price Index for September from the BLS. The consensus is for a 0.6% increase in PPI, and a 0.5% increase in core PPI.

8:30 AM ET: Retail sales for September will be released. The consensus is for a 0.2% decrease in retail sales.

8:30 AM ET: Retail sales for September will be released. The consensus is for a 0.2% decrease in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

8:30 AM ET: The New York Fed Empire State manufacturing survey for October. The consensus is for a reading of 27.0, down from 34.3.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for October).

Friday, October 08, 2021

AAR: September Rail Carloads and Intermodal Down Compared to 2019

by Calculated Risk on 10/08/2021 04:19:00 PM

From the Association of American Railroads (AAR) Rail Time Indicators. Graphs and excerpts reprinted with permission.

Rail traffic in September 2021 was a mix of good and could-be-better, reflecting continuing broad supply chain issues and an economy that doesn’t appear sure where it’s going.

U.S. intermodal volume in September 2021 was down 6.7% from last year and down 0.1% from September 2019. The smooth functioning of intermodal terminals depends on consistent freight outflows to make room for new freight inflows. Unfortunately, that’s not happening right now because of supply chain capacity constraints, with predicable impacts on intermodal. U.S. intermodal in 2021 through September was the second most ever, fractionally behind the first nine months of 2018.

Total U.S. carloads in September were up 4.3% over last year, their seventh straight monthly gain

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph from the Rail Time Indicators report shows the six week average of U.S. Carloads in 2019, 2020 and 2021:

U.S. railroads originated 1.17 million total carloads in September 2021, up 4.3% (47,858 carloads) over September 2020 but down 5.8% (71,773 carloads) from September 2019. Total carloads averaged 233,536 per week in September 2021. That’s more than in September 2020, but otherwise it’s the lowest weekly average for September in our data that go back to 1988.

The second graph shows the six week average (not monthly) of U.S. intermodal in 2019, 2020 and 2021: (using intermodal or shipping containers):

The second graph shows the six week average (not monthly) of U.S. intermodal in 2019, 2020 and 2021: (using intermodal or shipping containers):U.S. railroads originated 1.33 million intermodal containers and trailers in September 2021, down 6.7% from September 2020 and down 0.1% from September 2019. The 6.7% decline in September follows a 3.3% decline in August, which in turn followed a year of monthly intermodal gains. Intermodal volume averaged 265,705 containers and trailers per week in September 2021, the fewest since February 2021 (when a freakishly severe winter storm in Texas and surrounding states decimated rail traffic) and, before that, since July 2020.

October 8th COVID-19: Over 400 Million Doses Administered

by Calculated Risk on 10/08/2021 04:14:00 PM

The CDC is the source for all data.

According to the CDC, on Vaccinations. Total doses administered: 400,669,422, as of a week ago 393,756,866, or 0.99 million doses per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Week Ago | Goal | ||

| Percent fully Vaccinated | 56.3% | 55.7% | ≥70.0%1 | |

| Fully Vaccinated (millions) | 186.9 | 184.9 | ≥2321 | |

| New Cases per Day3 | 93,605 | 106,447 | ≤5,0002 | |

| Hospitalized3 | 62,456 | 72,704 | ≤3,0002 | |

| Deaths per Day3 | 1,421 | 1,554 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37 day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

IMPORTANT: For "herd immunity" most experts believe we need 70% to 85% of the total population fully vaccinated (or already had COVID).

KUDOS to the residents of Vermont that have achieved 70% of total population fully vaccinated: Vermont at 70.1%.

KUDOS also to the residents of the 13 states and D.C. that have achieved 60% of total population fully vaccinated: Connecticut at 69.3%, Maine, Rhode Island, Massachusetts, New Jersey, Maryland, New York, New Mexico, New Hampshire, Washington, Oregon, Virginia, District of Columbia and Colorado at 60.0%.

The following 21 states have between 50% and 59.9% fully vaccinated: California at 59.7%, Minnesota, Hawaii, Pennsylvania, Delaware, Florida, Wisconsin, Texas, Nebraska, Iowa, Illinois, Michigan, Kentucky, South Dakota, Arizona, Kansas, Nevada, Alaska, Utah, North Carolina and Ohio at 50.8%.

Next up (total population, fully vaccinated according to CDC) are Montana at 49.0%, Indiana at 48.9%, Missouri at 48.5% and Oklahoma at 48.3%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

2nd Look at Local Housing Markets in September: Memphis, Nashville, North Texas (Dallas), Northwest (Seattle), Sacramento and Santa Clara (San Jose)

by Calculated Risk on 10/08/2021 02:08:00 PM

Today, in the Newsletter: 2nd Look at Local Housing Markets in September Adding Memphis, Nashville, North Texas (Dallas), Northwest (Seattle), Sacramento and Santa Clara (San Jose)

Please subscribe!

Excerpt:

Excerpt:

Here is a summary of active listings for these housing markets in September. Inventory was up 0.1% in September MoM from August, and down 26.8% YoY.

Inventory in San Diego is at an all time low, whereas inventory in Denver and Sacramento is up more than double from the all time low earlier this year. Sacramento is one of the few areas with inventory up YoY.

Note: New additions to table in BOLD.

Q3 GDP Forecasts: Significant Downgrades

by Calculated Risk on 10/08/2021 12:34:00 PM

Here is a table of some of the forecasts over the last 2+ months. The significant downgrades during the quarter were primarily due to analysts initially underestimating the recent COVID wave, and also the impact of supply chain disruptions.

| Merrill | Goldman | GDPNow | |

|---|---|---|---|

| 7/30/21 | 7.0% | 9.0% | 6.1% |

| 8/20/21 | 4.5% | 5.5% | 6.1% |

| 9/10/21 | 4.5% | 3.5% | 3.7% |

| 9/17/21 | 4.5% | 4.5% | 3.6% |

| 9/24/21 | 4.5% | 4.5% | 3.7% |

| 10/1/21 | 4.1% | 4.25% | 2.3% |

| 10/8/21 | 2.0% | 3.25% | 1.3% |

From BofA Merrill Lynch:

We are taking down 3Q GDP tracking to 2% from 3.8% previously, reflecting a reassessment of equipment and inventories, and the likely soft retail sales data. [Oct 8 estimate]From Goldman Sachs:

emphasis added

Following today’s payroll miss and outright decline in education payrolls, we lowered our Q3 GDP tracking estimate by ¼pp to 3¼% (qoq ar). [Oct 8 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2021 is 1.3 percent on October 8 [Oct 8 estimate]

Reis: Apartment Vacancy Rate Decreased Sharply in Q3

by Calculated Risk on 10/08/2021 11:08:00 AM

Reis reported that the apartment vacancy rate was at 4.7% in Q3 2021, down from 5.3% in Q2, and down from 5.1% in Q3 2020. The vacancy rate peaked at 8.0% at the end of 2009, and bottomed at 4.1% in 2016.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the apartment vacancy rate starting in 1980. (Annual rate before 1999, quarterly starting in 1999).

Note: Reis is just for large cities.

Reis also reported the asking rents were up 7.5% year-over-year, compared to up 1.2% in Q2.

Reis also reported the asking rents were up 7.5% year-over-year, compared to up 1.2% in Q2.

For some cities, asking rents were up significantly more, especially in areas like Phoenix (up over 20% YoY), and many cities in California and Florida.

Apartment vacancy data courtesy of Reis.

Comments on September Employment Report

by Calculated Risk on 10/08/2021 09:12:00 AM

The headline jobs number in the September employment report was well below expectations, however employment for the previous two months was revised up significantly. The participation rate declined, and the unemployment rate decreased to 4.8%.

Leisure and hospitality gained 74 thousand jobs in September. In March and April of 2020, leisure and hospitality lost 8.2 million jobs, and are now down 1.6 million jobs since February 2020. So leisure and hospitality has now added back about 80% of the jobs lost in March and April 2020.

Construction employment increased 22 thousand, and manufacturing added 26 thousand jobs.

NOTE: State and Local education lost 161 thousand jobs, seasonally adjusted, versus expectations of a solid gain. This was a key contributor to the weak job report.

Earlier: September Employment Report: 194 Thousand Jobs, 4.8% Unemployment Rate

In September, the year-over-year employment change was 5.7 million jobs. This turned positive in April due to the sharp jobs losses in April 2020.

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.

This graph shows permanent job losers as a percent of the pre-recession peak in employment through the report today. (ht Joe Weisenthal at Bloomberg).

Earlier: September Employment Report: 194 Thousand Jobs, 4.8% Unemployment Rate

In September, the year-over-year employment change was 5.7 million jobs. This turned positive in April due to the sharp jobs losses in April 2020.

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.This graph shows permanent job losers as a percent of the pre-recession peak in employment through the report today. (ht Joe Weisenthal at Bloomberg).

This data is only available back to 1994, so there is only data for three recessions.

In September, the number of permanent job losers decreased to 2.251 million from 2.487 million in August.

In September, the number of permanent job losers decreased to 2.251 million from 2.487 million in August.

These jobs will likely be the hardest to recover, so it is a positive that the number of permanent job losers is declining rapidly.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The prime working age will be key as the economy recovers.

The 25 to 54 participation rate decreased in September to 81.6% from 81.8% in August, and the 25 to 54 employment population ratio was unchanged at 78.0% from 78.0% in August.

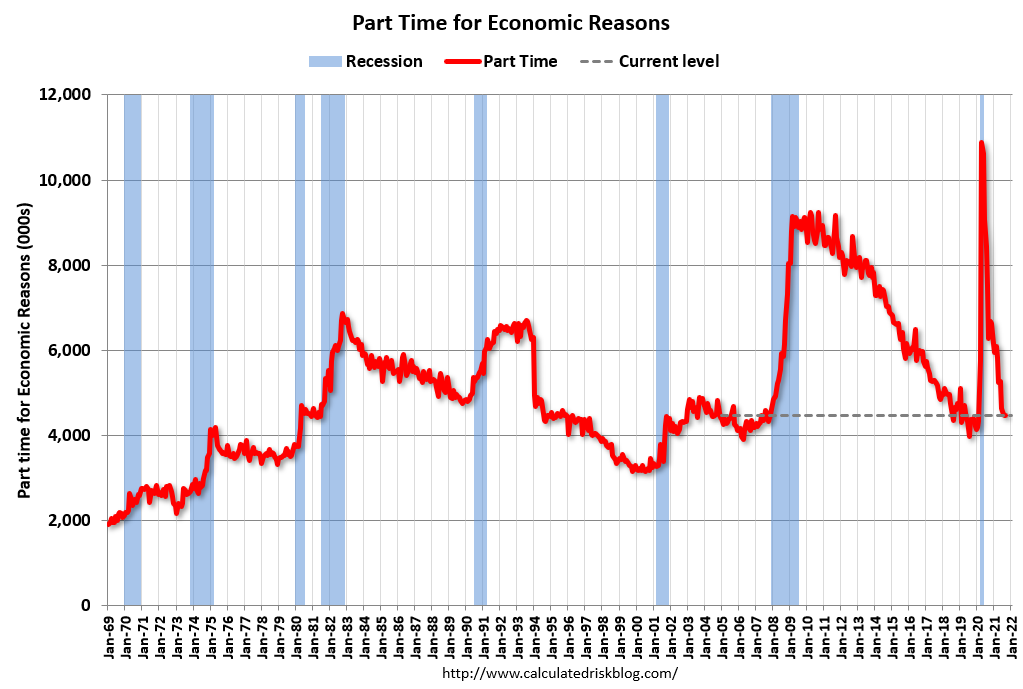

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"In September, the number of persons employed part time for economic reasons, at 4.5 million, was essentially unchanged for the second month in a row. There were 4.4 million persons in this category in February 2020. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons was essentially unchanged in September at 4.468 million from 4.469 million in August. This is back close to pre-recession levels.

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 8.5% from 8.8% in August. This is down from the record high in April 22.9% for this measure since 1994. This measure was at 7.0% in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 2.683 million workers who have been unemployed for more than 26 weeks and still want a job, down from 3.179 million in August.

This does not include all the people that left the labor force.

Summary:

The headline monthly jobs number was well below expectations, however the previous two months were revised up by 169,000 combined. And the headline unemployment rate decreased to 4.8%.

There was some good news - the decline in the unemployment rate, the decline in permanent job losers, and the decline in long term unemployed - however, there are still 5.0 million fewer jobs than prior to the recession, and overall this was a disappointing report, probably due to the sharp increase in COVID cases in September.

September Employment Report: 194 Thousand Jobs, 4.8% Unemployment Rate

by Calculated Risk on 10/08/2021 08:41:00 AM

From the BLS:

Total nonfarm payroll employment rose by 194,000 in September, and the unemployment rate fell by 0.4 percentage point to 4.8 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in leisure and hospitality, in professional and business services, in retail trade, and in transportation and warehousing. Employment in public education declined over the month.

...

The change in total nonfarm payroll employment for July was revised up by 38,000, from +1,053,000 to +1,091,000, and the change for August was revised up by 131,000, from +235,000 to +366,000. With these revisions, employment in July and August combined is 169,000 higher than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the year-over-year change in total non-farm employment since 1968.

In September, the year-over-year change was 5.7 million jobs. This was up significantly year-over-year.

Total payrolls increased by 194 thousand in August. Private payrolls increased by 317 thousand.

Payrolls for July and August were revised up 169 thousand, combined.

The second graph shows the job losses from the start of the employment recession, in percentage terms.

The second graph shows the job losses from the start of the employment recession, in percentage terms.The current employment recession was by far the worst recession since WWII in percentage terms, but currently is not as severe as the worst of the "Great Recession".

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate was declined to 61.6% in September, from 61.7% in August. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate was declined to 61.6% in September, from 61.7% in August. This is the percentage of the working age population in the labor force. The Employment-Population ratio increased to 58.7% from 58.5% (black line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate decreased in September to 4.8% from 5.2% in August.

This was well below consensus expectations, however July and August were revised up by 169,000 combined.

I'll have more later ...