RSS Feed

RSS Feed by Calculated Risk on 3/02/2016 06:44:00 PM

Wednesday, March 02, 2016

Thursday: Unemployment Claims, ISM non-Mfg Survey

From Matthew Graham at Mortgage News Daily: Mortgage Rates Pushing Important Boundary

Mortgage rates continued farther into to the highest levels since early February today. ...Thursday:

... 10yr Treasury yields ended the day at 1.84% and today's most prevalent conventional 30yr fixed rate quote is right on the edge of a move back up to 3.75% after a stable run at 3.625%.

• At 8:30 AM ET, the initial weekly unemployment claims report will be released. The consensus is for 270 thousand initial claims, down from 272 thousand the previous week.

• At 10:00 AM, Manufacturers' Shipments, Inventories and Orders (Factory Orders) for January. The consensus is a 2.0% increase in orders.

• Also at 10:00 AM, the ISM non-Manufacturing Index for February. The consensus is for index to decrease to 53.1 in February from 53.5 in January.

Fed's Beige Book: "Economic activity expanded in most Districts"

by Calculated Risk on 3/02/2016 02:36:00 PM

Fed's Beige Book "Prepared at the Federal Reserve Bank of Kansas City and based on information collected before February 22, 2016."

Reports from the twelve Federal Reserve Districts continued to indicate that economic activity expanded in most Districts since the previous Beige Book report. Economic growth increased moderately in Richmond and San Francisco and at a modest pace in Cleveland, Atlanta, Chicago, and Minneapolis. Philadelphia reported a slight increase in economic activity, and St. Louis described conditions as mixed. Most contacts in Boston cited higher sales or revenues than a year-ago but mixed results since the previous month. New York and Dallas described economic activity as flat, and Kansas City noted a modest decline in activity. Across the nation, business contacts were generally optimistic about future economic growth.And on real estate:

Residential real estate sales were up since the last report across all Districts, with the exception of New York and Kansas City where sales were somewhat weaker in part due to normal seasonal patterns. The Boston, Cleveland, St. Louis, and San Francisco Districts reported strong growth in sales, and contacts in Boston and Cleveland cited relatively mild winter weather as a positive contribution to growth. Low- to moderately-priced homes sold better than higher-priced homes in Cleveland, Kansas City, and Dallas. ... Residential construction generally strengthened since the previous survey period, with only Philadelphia and Kansas City reporting declines.Real Estate growth in most districts was decent ...

Districts characterized nonresidential real estate sales and leasing growth as flat to strong. Contacts in Cleveland cited growth in demand from the healthcare and higher education sectors and to a lesser extent the manufacturing, commercial real estate (excluding office buildings) and multifamily housing sectors. Commercial occupancy rates rose in San Francisco, spurring higher lease rates and additional construction projects. Commercial vacancy rates were nearing or below prerecession levels in Minneapolis despite significant new commercial real estate construction, and St. Paul saw more commercial net absorption in the last year than in the previous ten years combined. Similarly, industrial vacancy rates decreased across the Cleveland, St. Louis, and Dallas Districts. Demand for commercial real estate space grew robustly in Chicago across retail, industrial and office segments, but there was concern that the lack of commercial construction and increased demand would lead to space shortages and price bubbles. Commercial leasing activity in Boston was steady, and fundamentals remained strong. Richmond commercial leasing activity increased moderately for the retail market since the previous report, while activity in the office and industrial markets was tepid. Commercial rents increased in Philadelphia, and contacts in Atlanta noted generally improving rents as well as increased absorption.

emphasis added

Zillow Forecast: Expect "Modestly Slower Growth" in January for the Case-Shiller Indexes than in December

by Calculated Risk on 3/02/2016 11:22:00 AM

The Case-Shiller house price indexes for December were released last week. Zillow forecasts Case-Shiller a month early, and I like to check the Zillow forecasts since they have been pretty close.

From Zillow: January Case-Shiller Forecast: Modestly Slower Growth Expected

The December Case-Shiller indices grew at a pace in line with prior months, with all three headline indices showing annual appreciation above 5 percent per year. Zillow expects all three January Case-Shiller indices to show slower growth, with the 10-City Composite Index expected to register sub-5 percent annual growth for the first time in months.Although the 10-city and 20-city indexes will probably show modestly slower growth, this suggests the year-over-year change for the Case-Shiller National index will be slightly higher in January than in the December report.

The January Case-Shiller National Index is expected to gain another 0.6 percent in January from December, down from 0.8 percent growth in December from November. We expect the 10-City Index to grow 4.9 percent year-over-year, and the 20-City Index to grow 5.6 percent over the same period. The National Index looks set to begin 2016 up 5.6 percent year-over-year, the only instance in which monthly or annual growth next month is expected to surpass this month’s pace.

All SPCS forecasts are shown in the table below. These forecasts are based on [the] December Case-Shiller data release and the January 2016 Zillow Home Value Index (ZHVI), also released [last week]. The January Case-Shiller Composite Home Price Indices will not be officially released until Tuesday, March 29.

ADP: Private Employment increased 214,000 in February

by Calculated Risk on 3/02/2016 08:21:00 AM

Private sector employment increased by 214,000 jobs from January to February according to the February ADP National Employment Report®. ... The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.This was above the consensus forecast for 185,000 private sector jobs added in the ADP report.

...

Goods-producing employment rose by 5,000 jobs in February, just over a quarter of January’s upwardly revised 19,000. The construction industry added 27,000 jobs, which was slightly above January’s upwardly revised 26,000. Meanwhile, manufacturing lost 9,000 jobs, the second largest drop in five years.

Service-providing employment rose by 208,000 jobs in February, up from a downwardly revised 174,000 in January.

...

Mark Zandi, chief economist of Moody’s Analytics, said, “Despite the turmoil in the global financial markets, the American job machine remains in high gear. Energy and manufacturing remain blemishes on the job market, but other sectors continue to add strongly to payrolls. Full-employment is fast approaching.

The BLS report for February will be released Friday, and the consensus is for 190,000 non-farm payroll jobs added in February.

MBA: Mortgage Applications Decreased in Latest Weekly Survey, Purchase Applications up 27% YoY

by Calculated Risk on 3/02/2016 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 4.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 26, 2016. The previous week’s results included an adjustment for the President’s Day holiday.

...

The Refinance Index decreased 7 percent from the previous week, reaching its lowest levels since January 2016. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index increased 14 percent compared with the previous week and was 27 percent higher than the same week one year ago.

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) decreased to 3.83 percent from 3.85 percent, with points decreasing to 0.39 from 0.42 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

Refinance activity was higher in 2015 than in 2014, but it was still the third lowest year since 2000.

Refinance activity has picked up recently as rates have declined.

The second graph shows the MBA mortgage purchase index.

The second graph shows the MBA mortgage purchase index. According to the MBA, the unadjusted purchase index is 27% higher than a year ago.

Tuesday, March 01, 2016

Wednesday: ADP Employment, Beige Book

by Calculated Risk on 3/01/2016 07:01:00 PM

CR Note: Oops - lost a day somewhere ... corrected for Wednesday (HT Craig)

From Tim Duy: Dudley the Dove

The beleaguered manufacturing sector saw an uptick in February, at least according to the ISM report ... this information builds on the stronger consumer spending and inflation numbers we saw last week. Not to mention solid auto sales for February. The news is sufficiently good that Torsten Sløk of Deutsche Bank argues (via Business Insider) that the Fed should raise rates ...Wednesday:

I don't think the Fed will raise in March, nor do I think they should raise in March. I think the financial markets signaled fairly clear that further tightening now would be a mistake. The Fed would be wise to heed that call.

And, if New York Federal Reserve President William Dudley is any indication, they will heed that call. Indeed, he goes even further than me. Whereas yesterday I raised the possibility of a "hawkish pause" at the March meeting where the Fed revives the balance of risks with an upside bias, he opens the door to the opposite.

...

Bottom Line: The Fed will take a pass on the March meeting. Whether the statement is dovish, neutral, hawkish is the key question. Dudley opens up the possibility of a not just a neutral statement, but a dovish one. My sense is that this is shaping up to be a very contentious meeting as participants struggle with the question of exactly which data are they dependent upon.

• At 7:00 AM ET, the The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:1`5 AM, the ADP Employment Report for February. This report is for private payrolls only (no government). The consensus is for 185,000 payroll jobs added in February, down from 206,000 in January.

• At 2:00 PM, the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

U.S. Light Vehicle Sales at 17.43 million annual rate in February

by Calculated Risk on 3/01/2016 03:06:00 PM

Based on an estimate from WardsAuto, light vehicle sales were at a 17.43 million SAAR in February.

That is up about 7% from February 2015, and mostly unchanged from the 17.45 million annual sales rate last month.

Click on graph for larger image.

This graph shows the historical light vehicle sales from the BEA (blue) and an estimate for February (red, light vehicle sales of 17.43 million SAAR from WardsAuto).

This was below the consensus forecast of 17.6 million SAAR (seasonally adjusted annual rate).

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

Note: dashed line is current estimated sales rate.

Note: dashed line is current estimated sales rate.

Although slightly below expectations, sales are off to a solid start in 2016.

Construction Spending increased 1.5% in January

by Calculated Risk on 3/01/2016 10:59:00 AM

The Census Bureau reported that overall construction spending increased 1.5% in January compared to December:

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during January 2016 was estimated at a seasonally adjusted annual rate of $1,140.8 billion, 1.5 percent above the revised December estimate of $1,123.5 billion. The January figure is 10.4 percent above the January 2015 estimate of $1,033.3 billion.Both private and public spending increased in January:

Spending on private construction was at a seasonally adjusted annual rate of $831.4 billion, 0.5 percent above the revised December estimate of $827.3 billion. ...

In January, the estimated seasonally adjusted annual rate of public construction spending was $309.4 billion, 4.5 percent above the revised December estimate of $296.2 billion.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Private residential spending has been increasing, but is 36% below the bubble peak.

Non-residential spending is only 4% below the peak in January 2008 (nominal dollars).

Public construction spending is now 5% below the peak in March 2009. The sharp increase in public spending in January was due to more spending on streets and highways (up 34% year-over-year).

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.On a year-over-year basis, private residential construction spending is up 8%. Non-residential spending is up 11% year-over-year. Public spending is up 13% year-over-year.

Looking forward, all categories of construction spending should increase in 2016. Residential spending is still very low, non-residential is increasing (except oil and gas), and public spending is also increasing after several years of austerity.

This was well above the consensus forecast of a 0.5% increase for January, and construction spending for November and December were revised up.

ISM Manufacturing index increased to 49.5 in February

by Calculated Risk on 3/01/2016 10:04:00 AM

The ISM manufacturing index indicated contraction in February. The PMI was at 49.5% in February, up from 48.2% in January. The employment index was at 48.5%, up from 45.9% in January, and the new orders index was at 51.5%, unchanged from January.

From the Institute for Supply Management: February 2016 Manufacturing ISM® Report On Business®

Economic activity in the manufacturing sector contracted in February for the fifth consecutive month, while the overall economy grew for the 81st consecutive month, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®.

The report was issued today by Bradley J. Holcomb, CPSM, CPSD, chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee. "The February PMI® registered 49.5 percent, an increase of 1.3 percentage points from the January reading of 48.2 percent. The New Orders Index registered 51.5 percent, the same reading as in January. The Production Index registered 52.8 percent, 2.6 percentage points higher than the January reading of 50.2 percent. The Employment Index registered 48.5 percent, 2.6 percentage points above the January reading of 45.9 percent. Inventories of raw materials registered 45 percent, an increase of 1.5 percentage points above the January reading of 43.5 percent. The Prices Index registered 38.5 percent, an increase of 5 percentage points above the January reading of 33.5 percent, indicating lower raw materials prices for the 16th consecutive month. Comments from the panel indicate a more positive view of demand than in January, as 12 of our 18 industries report an increase in new orders, while four industries report a decrease in new orders."

emphasis added

Click on graph for larger image.

Click on graph for larger image.Here is a long term graph of the ISM manufacturing index.

This was above expectations of 48.5%, but still suggests manufacturing contracted in February.

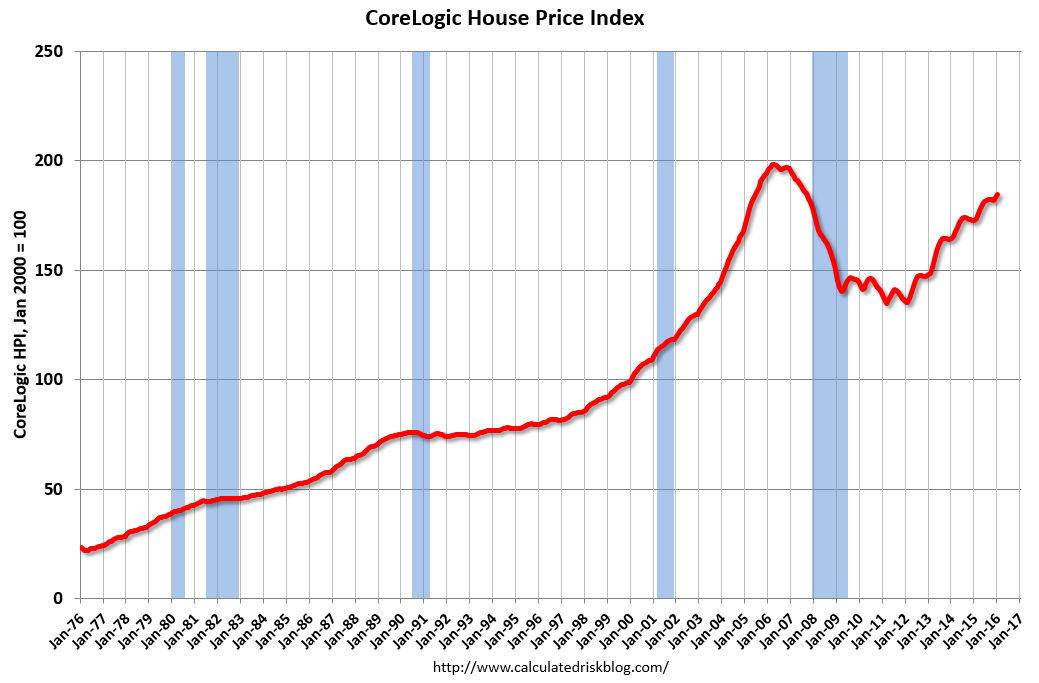

CoreLogic: House Prices up 6.9% Year-over-year in January

by Calculated Risk on 3/01/2016 09:29:00 AM

Notes: This CoreLogic House Price Index report is for January. The recent Case-Shiller index release was for December. The CoreLogic HPI is a three month weighted average and is not seasonally adjusted (NSA).

From CoreLogic: CoreLogic US Home Price Report Shows Home Prices Up 6.9 Percent Year Over Year in January 2016

Home prices nationwide, including distressed sales, increased year over year by 6.9 percent in January 2016 compared with January 2015 and increased month over month by 1.3 percent in January 2016 compared with December 2015, according to the CoreLogic HPI.

...

“While the national market continues to steadily improve, the contours of the home price recovery are shifting,” said Dr. Frank Nothaft, chief economist for CoreLogic. “The northwest and Rocky Mountain states have experienced greater appreciation and account for four of the top five states for home price growth.”

emphasis added

Click on graph for larger image.

Click on graph for larger image. This graph shows the national CoreLogic HPI data since 1976. January 2000 = 100.

The index was up 1.3% in January (NSA), and is up 6.9% over the last year.

This index is not seasonally adjusted, and this was a solid month-to-month increase.

The second graph shows the YoY change in nominal terms (not adjusted for inflation).

The YoY increase had been moving sideways over the last year, but has picked up a recently.

The YoY increase had been moving sideways over the last year, but has picked up a recently.The year-over-year comparison has been positive for forty seven consecutive months.